Analytical Products and Services focused on individual bonds, bond portfolios, bond swap transactions, and company wide interest rate and liquidity risk.

Founded in 1996, R2Metrics provides managers of interest rate risk with fast, reliable and inexpensive analytical tools and reports. We specialize in measuring interest rate risk and reward in individual bonds, bond portfolios, bond swap transactions, and company balance sheets. Our analytical tools are highly customizable and we normally model 100% of the items in a bond portfolio or on a company balance sheet.

Read More

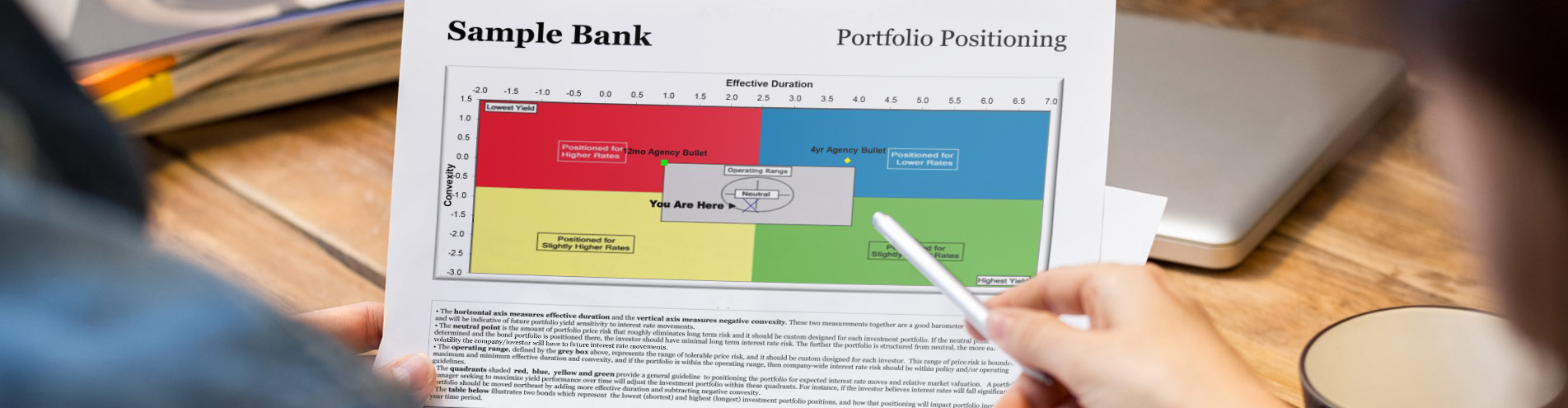

BondRisk is a comprehensive fixed income portfolio analytics tool for portfolio managers, securities dealers, and related entities. It provides in-depth interest

Read More

SwapRisk is a robust analytical tool which estimates expected portfolio book yields and income generated by one portfolio composed of prospective

Read More

Allows for aggregated monitoring of client holdings and includes an alert for maturing and called securities as well as search capabilities

Read More

FAS 107 requires most entities to disclose the fair value of financial instruments (cash, evidence of an ownership in an entity,

Read More

Proprietary Asset/Liability Model designed to meet the Interest Rate Risk (IRR) modeling requirements of mid-market and smaller Financial Institutions (FI). Incorporates

Read More

As an independent ALM provider, R2Metrics is one of the few firms able to provide a 3rd party parallel ALM simulation,

Read More

205-329-1275

205-329-1275

100 Corporate Ridge, Ste 201 Birmingham, AL 35242

100 Corporate Ridge, Ste 201 Birmingham, AL 35242